SSIS College Spotlight: Financial Terms, Tools, and Tips

volume 2, issue 1. Fall 2016

volume 2, issue 1. Fall 2016

Dear Seniors and Families,

This Spotlight focuses on college finances.

One of the things that can be especially exasperating with the college application process is that each college and university has its own mechanisms for determining your financial package. In so many instances, you simply won’t know how much a college truly will cost until you receive an offer. However, you can make a “best guess” if you understand the financial language these schools employ and take advantage of online and other resources.

As always, feel free to make use of the SSIS College Counseling office and me! I am available by appointment during Flex and after school.

Best always,

Caroline

Your College Counselor

_________________________________

COST OF ATTENDANCE

Colleges publish the cost of attendance (tuition, room and board, books and supplies, student fees, transportation, and living expenses. Depending on the school and where it is located, the total cost of attendance (COA) can range widely. For example, for the 2017-2018 school year, Western Washington University’s COA comes to $22,828 and Harvey Mudd College’s COA is $71, 917.

Before you go into sticker shock, consider that three-quarters of Harvey Mudd students attend with substantial financial support from both college scholarships and grants as well as from federal and state government funds. Harvey Mudd’s policy is to meet 100% of a family’s demonstrated need. The comparison with Western Washington Scholarships is intriguing—a high school student with great grades, scores, and other aptitudes who is accepted at both schools may not have to make a choice on financial grounds.

FINANCIAL PACKAGE

Your financial package may include one or several of the following:

- merit scholarships and grants (these are gifts and do not need to be repaid)

- need-based scholarships and grants (these are gifts and do not need to be repaid)

- work-study (on-campus jobs)

- loans (some loans may be interest free, deferred until graduation, and provided by the school, other loans may be offered by the government at a low interest rate; expensive private loans are explicitly discouraged)

100% DEMONSTRATED NEED

Many colleges and universities are now using this language to convey that they are prepared to make their college a reality for you by meeting you where you are financially.

There are three primary categories:

- * 100% demonstrated need, regardless of family income — without loans

- * 100% demonstrated need for families within a specific income range — without loans

- * 100% demonstrated need, but may include loans

Here is a link to a September 2015 list of schools offering 100% demonstrated need by category; here is an August 2016 list (each school listed has a category notation, but the list itself is organized alphabetically)

EXPECTED FAMILY CONTRIBUTION

Colleges and universities determine “demonstrated need” by analyzing the financial data you provide them with the FAFSA (Free Application for Federal Student Aid) and/or CSS (College Scholarship Service) financial aid forms. These forms establish your personal financial profile and therefore determine your expected family contribution.

FAFSA

The Free Application for Federal Student Aid (FAFSA) functions like a national clearing house for financial aid. Because the FAFSA application involves verification of prior year household and income data from the IRS, most colleges depend on it as a reliable basis to ascertain your expected family contribution. Even if you do not qualify for federal or state financial aid, it is wise to complete the FAFSA. Many colleges use FAFSA information to help determine whether you might qualify for other cost reductions such as grants, scholarships, and work-study.

CSS

The College Board provides a College Scholarship Service (CSS) that many of the nation’s most selective colleges and universities also require. Its purpose is to help them determine their allocation of non-government financial aid such as the college’s own grants, scholarships, and loans. The CSS application demands more detailed information than the FAFSA, including whether you own a home, and is specific to each college to which you apply. This feature allows college financial aid officers greater discretion than is possible with only the FAFSA. There is a small application fee, but some families may qualify for a fee waiver.

FULL RIDE

Exceptional high school scholars who have demonstrated leadership, innovation, service or other such qualities have the opportunity to vie for merit scholarships that cover full tuition or even a full-ride (tuition plus other expenses). Here is a 2015 list of 79 colleges with full-ride scholarships. Check individual colleges for their financial aid policies and opportunities. There are many more than 79 schools offering full-tuition or other significant merit aid that celebrates any number of capacities and talents, including the arts and athletics, not just test scores and academics.

PELL GRANT

Students with considerable financial need may qualify for a Pell Grant—a federally funded grant that does not have to be paid back. The maximum award is $5,815 for 2016-2017.

ESTIMATED NET COST

Subtracting the expected family contribution and financial aid package from the total COA reveals your estimated net cost. College Kickstart has published a blog that illustrates by example how to make sense of financial aid packages. Because colleges have different endowments and scholarship funds, and they use CSS and FAFSA information differently, their calculations of your expected family contribution can vary as will their financial aid offers.

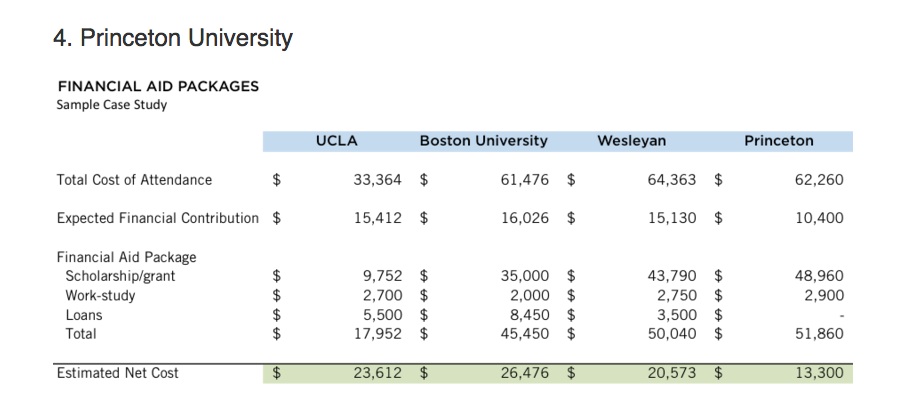

HERE IS AN EXAMPLE COMPARING UCLA, BOSTON U., WESLEYAN, AND PRINCETON:

From College Kickstart

The premise of the case study above is that the student is a California resident and therefore has in-state tuition at UCLA. She is an excellent student who was accepted by all four selective schools. The family’s household includes two parents and a sibling, the parents have a combined income of $110,000 with $50,000 in savings, and the student has no assets. The schools themselves are committed to meeting 100% demonstrated need, but one can afford to do so without loans as well as estimate a significantly lower EFC for the family. Your takeaway: read the details of your package carefully. The big difference between Wesleyan and UCLA is that UCLA would cost $282 more in cash and $2,000 more in loans, and save $50 in work-study. With its long history of developing its endowment and other financial resources, Princeton is the least expensive option.

TOOLS:

- College website financial aid pages

- College net price calculators (for example, here is the Princeton U. Estimator)

- FAFSA and CSS websites

- For FAFSA, you will need a FAFSA ID and you will want to use the IRS Data Retrieval Tool.

- Scholarship websites, including national scholarships and those targeting Washington State residents (please consult the Spotlight focused on scholarships).

- For income under $50,000 use ScholarMatcher to find colleges that retain and graduate students on time, offer generous financial aid, and provide ample student affairs services.

TIPS:

- FAFSA and CSS applications are published on October 1st; do not wait to complete these. Most states, including Washington, disburse state financial aid on a first-come, first-serve basis.

- FAFSA considers parent and student income, size of household, number of children in college, assets other than a primary resident, and excludes retirement savings and some non-discretionary expenses such as taxes and medical expenses.

- Federal and individual college formulas can vary, for example: federal methods exempt the primary residence altogether whereas colleges may consider home equity; federal methods consider only custodial parent (and spouse) assets whereas individual colleges demand information from the non-custodial parent (and spouse) as well; and, individual colleges tend to use modified income assessment rates that can help relieve the financial burden of middle-class families.

- Always apply to a public university in your state, then take a look at other options!